To download a PDF version of the declaration, click here.

BEFORE THE POSTAL REGULATORY COMMISSION

WASHINGTON, D.C.

20268-0001

STATUTORY REVIEW OF THE SYSTEM FOR REGULATING RATES AND CLASSES FOR MARKET DOMINANT PRODUCTS

Docket No. RM2017-3

DECLARATION OF MICHAEL NADOL ON BEHALF OF ALLIANCE OF NONPROFIT MAILERS, ASSOCIATION FOR POSTAL COMMERCE, AND MPA—THE ASSOCIATION OF MAGAZINE MEDIA

(March 20, 2017)

I. Background and Assignment

I, Michael Nadol, am President of PFM Group Consulting, LLC and a shareholder and Managing Director in the PFM Group of affiliated companies, which provide financial and management advisory services to public sector entities nationwide. In over 17 years with the PFM Group, I have advised state and local governments and federal agencies on a broad range of management and budget issues, including recovery from fiscal distress, multi-year financial planning, retiree benefits, and public employee compensation. My clients have included a majority of the ten largest U.S. cities by population, as well as the states of New York, Pennsylvania, Kentucky, Tennessee, Washington, New Jersey, and Delaware. With PFM, I have testified as an expert witness regarding financial management and/or compensation comparability in Federal District Court, before two Presidential Emergency Boards convened under the Railway Labor Act, and in public employee interest arbitration proceedings in nine states.

Prior to joining PFM, I worked in the public and nonprofit sectors for 14 years, with eight of those years spent in a range of management and budget positions with the City of Philadelphia, Pennsylvania, including Director of Finance and Director of Labor Relations. I have also served on the faculty of the University of Pennsylvania’s master of public administration program since 1997, and am an appointed adviser to the Government Finance Officers Association national committee on Governmental Budgeting and Fiscal Policy. I hold a bachelor’s degree, summa cum laude, from Yale University and a master’s degree in governmental administration from the University of Pennsylvania, Fels Institute of Government.

A more detailed summary of my training and experience is provided in Exhibit A.

For this report, I was engaged by MPA – Association of Magazine Media to provide research, analysis, and development of an expert report for the Postal Regulatory Commission 10-Year Review of System of Regulating Rates. For this report, I was asked to focus specifically on evaluating the condition of key components of the United States Postal Service (“USPS” or “Postal Service”) balance sheet, particularly as related to retiree benefits, and to assess major drivers of the USPS operating budget, notably employee compensation.

To conduct this review, I evaluated prior reports and testimony from the USPS itself, U.S. Government Accountability Office (“GAO”), and the USPS Office of Inspector General (“OIG”), and conducted up-to-date original analysis based on data from the U.S. Bureau of Labor Statistics (“BLS”), major credit rating agencies, and a broad range of primarily governmental sources. For some analysis, professional staff under my direction assisted in data collection, review, calculations, and quality assurance. In all cases, I have closely reviewed such supporting work directly. The information on which I have relied is footnoted throughout this report, with key datasets and calculations provided in an accompanying Library reference.

II. Overview of Findings

My review and analysis indicates that the USPS is significantly better positioned than most other large, public sector organizations to manage the long-term requirements of funding retiree benefit liabilities. With comparatively strong funded levels, the Postal Service can continue to strengthen this component of its balance sheet over a multi-decade period with no near-term – or even intermediate-term – budget risk.

At the same time, the USPS also holds significant opportunities to improve its future operating budgets by further restructuring its approach to personnel costs – the single largest driver of overall Postal Service operating expenditures. As long acknowledged, and confirmed through updated analysis within this report, the USPS provides its employees with a substantial total compensation premium above what is typically provided for comparable levels of work in the private sector of the economy. With multiple tools available to contain and even reduce these costs going forward, the Postal Service has ample opportunity to manage against and within revenue restraints.

Balance Sheet and Retiree Benefit Liabilities

The USPS has regularly cited balance sheet concerns, associated primarily with retiree benefit liabilities, as a significant challenge to its financial health. These liabilities have been addressed in numerous reports by the OIG and GAO, and statutory mandates for retiree healthcare prefunding have been the primary driver of recent USPS operating net losses and non-payments characterized as defaults.

While a sound funding approach for long-term liabilities is indeed important, a more comprehensive evaluation of the underlying USPS balance sheet condition leads to a very different conclusion regarding the current Postal Service fiscal condition than the recent language of net losses and defaults would connote. In particular, it is critical to recognize that the statutorily established targets for USPS retiree healthcare prefunding that drove recent operating losses were not actuarially determined, but were instead substantially frontloaded and inconsistent with mainstream retiree healthcare funding practices.

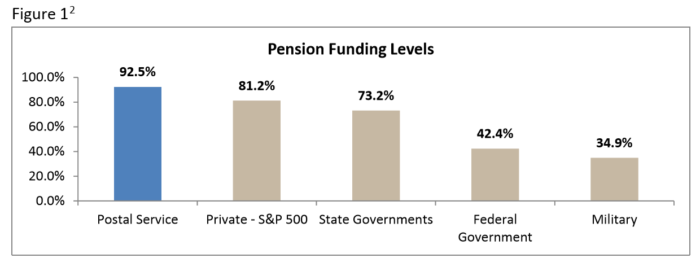

In fact, when viewed on a comparative basis, the USPS is currently better positioned than most other entities – both public and private – with regard to its retiree benefit obligations. Looking at reported actuarial funded levels as of FY2014 (the most recent year for which comparative data are broadly available), the Postal Service’s 92.5% pension funding level was in far stronger condition than most state and local government plans, as well as the federal government overall, and also well above the private sector standards established under the Pension Protection Act of 2006 for determining a plan to be “at risk” or “endangered.” [1] Likewise, for retiree healthcare, while the USPS is funded at a lower actuarial level than for pensions at approximately 50%, most private employers, the federal government, and many state and local governments have yet to prefund this benefit at all.

Figure 1 [2]

Further, these USPS nominal funded levels are actuarially calculated based on more conservative assumptions than used by most comparable plans, driven by federal constraints on investment practices associated with lower investment risk. For example, the aggregate Postal Service retirement plans, if estimated based on a 7.0% investment return assumption instead of the current 5.25% for pensions and 3.9% for retiree healthcare, would have total assets in excess of total liabilities.

Reasonable, partial steps forward have been proposed by USPS management and other stakeholders to mitigate the ongoing financial burden of retiree benefit liabilities. Postal Service proposals and pending federal legislation – to require Medicare participation for USPS retirees (given that the Postal Service fully contributes into the Medicare program), to calculate USPS liabilities using Postal Service-specific assumptions rather than federal government-wide demographics, and to allow for a broader range of investment options – could substantially reduce, if not eliminate, both the current unfunded liabilities and the budget pressure resulting in operating net losses.

As such opportunities are pursued, it is important to recognize that the funding of retiree benefit liabilities is a long-term challenge for most major public employers and for those corporations still offering defined benefits at all. This challenge is generally expected to take decades to address and correct under standard funding approaches. At the USPS, with substantially better funding levels than most other public and private employers, there is similarly no immediate solvency concern – even with no reforms. As of September 30 2016, the USPS had a total of nearly $338.4 billion in prefunding set aside for pension and retiree healthcare liabilities. At this level of funding, estimates detailed later within this report project that the Postal Service could make no further contributions into these accounts for the next ten years, adopt no further benefit or actuarial reforms, fully pay all current obligations out of these funds, and still have $243.3 billion in remaining assets available as of September 30, 2027Expense, September 12, 2016, Standard & Poor’s RatingsDirect: Pensions and OPEBs are Heading Into The Sunset, A Half-Trillion Dollars Short, June 17, 2015.

Given the available and viable options to reduce these obligations, viewed in tandem with the very long-term nature of these challenges and the Postal Service’s comparatively strong progress toward addressing them, the USPS should focus first on maximizing its opportunities to lower the size of these liabilities rather than prematurely increasing and destabilizing its rate structure to fund what is currently projected. There is no immediate “crisis,” the Postal Service is on a path toward incrementally resolving the multi-decade challenge that does exist, and achievable liability reduction measures could dramatically reduce these long-term funding needs to obviate any need for increased funding well before these liabilities generate true, near-term solvency pressure.

Looking at the USPS balance sheet beyond retiree liabilities, the Postal Service’s real estate assets have also been estimated to hold substantially greater value than accounting treatments of these assets would suggest. When viewed from a fair market value perspective, these assets provide additional strength to the USPS balance sheet, reflecting greater financial health and flexibility than cited book value indicates – in turn, providing a substantial and under-recognized safety net against any long-term industry and business risks faced by the USPS.

Finally, with regard to balance sheet considerations, it may be noted that limitations of the current USPS financial statements almost certainly understate the strength of the Postal Service position in the two respects noted above that have yet to be accurately quantified. Again, USPS retiree benefit levels are valued based on U.S. government-wide economic and demographic assumptions that the Postal Service estimates to significantly overstate its liabilities. Second, the fair market value of the USPS real estate assets has only been estimated using broad, 2012 trend factors. Before significantly increasing funding to address perceived balance sheet concerns, it would be beneficial to first more accurately assess this position, along with pursuing available liability reduction opportunities.

[1] Congressional Research Service, “Summary of the Pension Protection Act of 2006,” October 23, 2006.

[2] Sources: USPS Report Form 10-K, Civil Service Retirement and Disability Fund 2015 Annual Report, U.S. Military Retirement Fund Audited Financial Report 2015, Standard & Poor’s RatingsDirect: U.S. State Pensions: Weak Market Returns Will Contribute To Rise In

Operating Costs and the Postal Service Compensation Premium

Postal Service operations are labor-intensive, and employee wages and benefits are the single largest driver of USPS operating costs. According to the 2016 Report on Form 10-K of the USPS, total compensation costs represented 78.6% of total operating expenses for FY2016 – more than $60 billion and over three-quarters of all spending. [3] The simple equation that drives such overall workforce operating costs is the average cost per employee multiplied by the total number of employees. As further detailed in subsequent sections of this report, the USPS has significant opportunities to manage cost pressures from both of these factors to work within its revenue framework going forward.

With regard to cost per employee, the USPS continues to provide a substantial wage and benefit compensation premium well above the policy directive of the Postal Reorganization Act of 1970, 39 U.S.C. § 1003(a) (“PRA”), that the Postal Service shall:

“…maintain compensation and benefits for all officers and employees on a standard of comparability to the compensation and benefits paid for comparable levels of work in the private sector of the economy.”

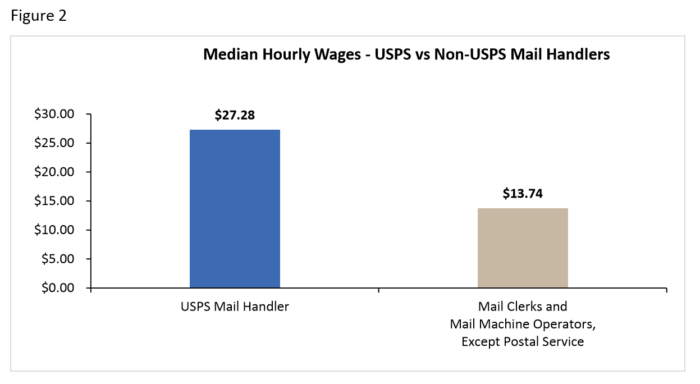

As further detailed later in this report, using BLS Occupational Employment Statistics (“OES”) data, I compared average Postal Service compensation across major USPS occupations to related occupations in the broader private sector. This analysis indicated a substantial wage premium for Postal Service employees – as shown in Figure 2 below comparing median hourly wages for Postal Service and non-USPS mail handlers as of May 2015. Further, parallel comparisons of USPS benefits relative to private sector norms identified additional advantages in the Postal Service overall compensation structure.

In turn, the existence of this substantial compensation premium provides the opportunity for future moderation of the largest Postal Service cost category, and even substantial reductions as needed, without adversely impacting the ability to recruit and retain a quality workforce.

Under the existing rate system in place since the passage of the Postal Accountability and Enhancement Act (“PAEA”), the Postal Service has achieved some savings through measures such as reduction in the size of its overall workforce, and expanded use of flexible, non-career (Tier 2) employees paid at levels with less of a premium above comparable private sector pay rates. Although higher-paid, incumbent career (Tier 1) employees have experienced little or no cost containment in compensation, the pay scales for Tier 2 employees newly hired since 2010- 2013 have also been moderately lowered.

Across these various savings approaches, however, the Postal Service’s actions have been limited and partial, and have slowed – or even reversed direction – within the past several years. Going forward, remaining opportunities for cost reduction and containment continue to hold significant untapped potential.

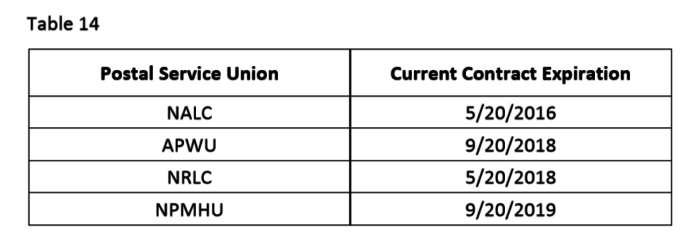

As of March 2017, none of the four major USPS unions have a collective bargaining agreement extending beyond 2019. Accordingly, the great majority of the time period to be covered under the next ten-year rate system will take place under collective bargaining agreements yet to be negotiated. These agreements determine much of the existing Postal Service compensation structure. Specific opportunities prospectively include:

- Contain future growth in compensation for the long-term, Tier 1 career service employees who benefit from the largest wage and benefit premium. As will be further detailed, this large cohort has continued to experience pay schedule increases in excess of the growth in consumer prices and federal pay over the past decade of contract periods.

- Further restructure the compensation for new career service hires to work under a more affordable, permanent second tier. Despite some adjustments for new Tier 1 workers hired since 2010-2013, all career service compensation remains well above market levels. Such permanent two-tier structures are a common approach for industries adjusting to changing market and economic realities.

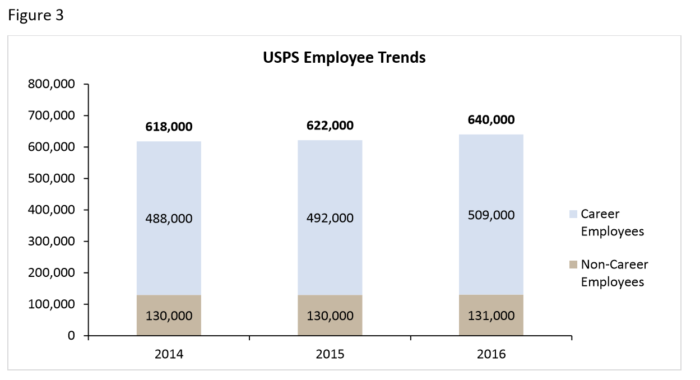

- Expand the use of Tier 2 non-career service employment to provide greater workforce flexibility and cost relief. Current Tier 2 pay rates are comparatively well aligned with the broader labor market, and could form the basis for both permanent and temporary second tiers going forward. For example, Tier 2 Mail Handlers earned between $14.37 and $15.15 per hour in May 2015, much more closely aligned with the $13.74 median hourly wage for comparable workers outside of the Postal Service previously referenced than the $27.28 median wage for Tier 1 USPS Mail Handlers. In practice, however, the percentage of Tier 2 employees in the overall Postal Service workforce actually declined from 2014 to 2016. As shown in Figure 3 below, of 22,000 net positions added from 2014 to 2016, 21,000 (95.5%) were in Tier 1 career jobs.

- Address the high cost of benefits. While some of the generous USPS healthcare and retirement benefits are required under current law, the Postal Service can continue to collectively bargain limitations on its employer share of the contributions toward healthcare premiums. Although partial progress has been made in this direction, the Postal Service still provides a more generous subsidy than the rest of the federal government contributes toward its own employees in the same system. In addition, the Postal Service collective bargaining agreements continue to feature paid leave benefits well in excess of private sector norms, which drive higher staffing levels and costs.

- With regard to the total number of USPS employees, headcount can also be adjusted as needed to help manage changes in demand, as done from 2006 to 2014 under the existing rate system. Overall, however, not only have USPS position levels actually increased since 2014, but the GAO has also recently testified that the Postal Service “has no current plans to initiate new major initiatives to achieve cost savings in its operations.”[4] While it is concerning that further progress toward increased efficiency and productivity is not underway, this set of circumstances also presents an opportunity going forward. If the USPS is challenged to drive toward greater economies and provided economic incentives to do so, the staffing reductions that can be advanced through management, technology, and/or service adjustments would all generate savings relative to the Postal Service’s current projections.

In total, reining in the general Postal Service compensation premium could make available billions of dollars in additional compensation capacity that could be redeployed to help address other needs – whether for capital investment, rate relief, and/or to fund any long-term costs for retiree benefit obligations that cannot be otherwise resolved.

Finally, to provide a framework for advancing the above opportunities in ways consistent with the USPS statutory mandate to achieve private sector compensation comparability, it is important that the Postal Service not be handed a “blank check” for funding continued wage and benefit premiums and career staffing increases. While the achievement of workforce cost containment over the past ten years has only been partial, what progress has been made has occurred while subject to pricing limitations that provide some meaningful counterbalance in collective bargaining and interest arbitration. With retention of a reasonable rate cap, the USPS and its employee representatives will have a better framework and incentives in place to bargain toward compensation and benefits more consistent with the PRA policy directives for private sector comparability. Absent any such counterweight, however, the incentives for labor cost moderation will be substantially eroded.

Each of these considerations is addressed in greater detail in the sections that follow.

[3]2016 USPS Report on Form 10-K, page 12.

[4] GAO-17-404T, “USPS Key Considerations for Restoring Fiscal Sustainability,” February 17, 2017, page 10.

III. Current Postal Service Pension and Retiree Benefit Liabilities are Comparatively Well Funded

Pensions

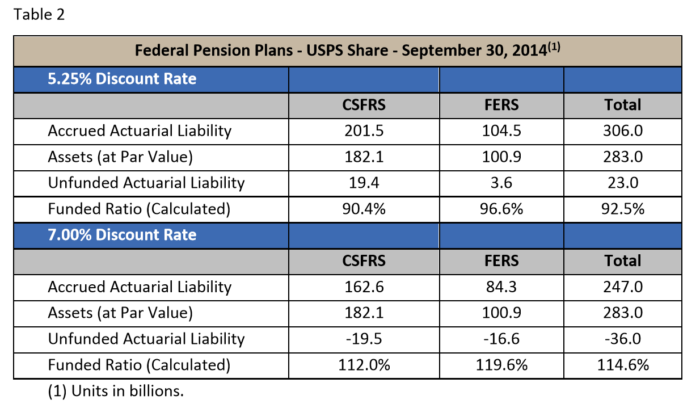

By any industry standard, the financial condition of USPS pensions is comparatively strong, as illustrated in Figure 1 within the “Overview of Findings” section of this report. As of September 30, 2014 (FY2014), the most recent date for which comparative information across a wide range of plans elsewhere is available, the funded level of the Postal Service component of the Civil

Service Retirement System (“CSRS”) was 90.4% and the Postal Service component of the Federal Employees Retirement System (“FERS”) was funded at 96.6%. In the aggregate, the USPS pensions were nearly 92.5% funded.

This USPS funded ratio was higher than the funded level of the rest of the CSRS and FERS plans, the United States military plan, and the averages for all state government and S&P 500 plans, as further detailed below:

- In the federal CSRS program,[5] the overall FY2014 funded level was 31.0%, inclusive of USPS participation. Without the Postal Service component, the FY2014 funding level was only 17.6%. In the FERS program, the overall funded ratio was 91.2%, and was 90.0%

without USPS participation. In the aggregate, these two major federal pension programs were 51.6% funded overall, and only 42.4% funded without the Postal Service’s participation. - The U.S. Military Retirement Fund reported just a 34.9% funded ratio for FY2014. [6]

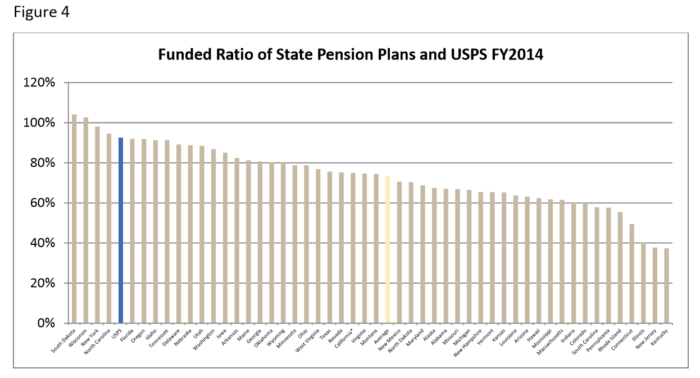

- Among state and local governments, the funded ratio for the Public Plan dataset onsisting of large local plans and all state plans was 74.1% in FY2014.[7] The average funded ratio of the proportionate liability of state governments specifically was 73.2%.[8] As shown in Figure 4, the USPS funded ratio was higher than that of 46 states in FY2014, even though the Postal Service uses more conservative actuarial assumptions, as further outlined in Section IV of this report.

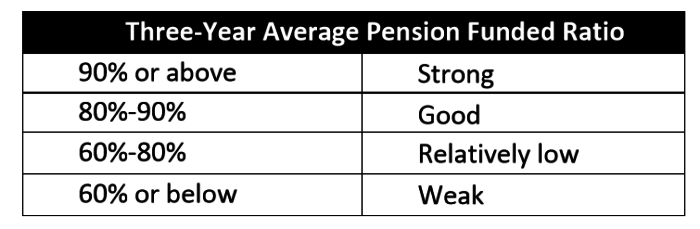

Credit rating agencies analyzing the state and local sector consider a broad range of factors regarding pension funding in their evaluations, including the reasonableness of actuarial assumptions, funding discipline, and funding capacity. In the context of this broader framework,

Standard & Poor’s has cited the following general standards for categorizing state government Pension Funded Ratios: [9]

- In the private sector, 329 of the S&P 500 companies had defined benefit pension plan liabilities in FY2014. The overall funded ratio for these plans was 81.2%. As governmental plans, the federal CSRS and FERS are not subject to the rules and regulations of the Pension Protection Act of 2006. For the private sector, this legislation established standards pursuant to which plans are subject to more stringent requirements for plan administration. In conjunction with such requirements, the general threshold for a single-employer plan to be considered “at-risk” and for a multi-employer plan to be categorized as “endangered” would be to fall below an 80% funded level.

The aggregate CSRS and FERS funded ratio of 92.5% for FY2014 was used above primarily because that is the most recent year for which comparative information is broadly available. More recent financial statements report that this ratio has improved to 93.2% as of FY2015 and is estimated to stay consistent at 93.1% in FY2016. While full funding remains an appropriate long-term goal, the Postal Service continues to be exceptionally well-positioned along this path.

[5] Table 1A, page 28, Civil Service Retirement and Disability Fund Annual Report, FY15; Statement of Postmaster General and CEO Megan J Brennan before the House Oversight and Government Reform Committee Hearing “Accomplishing Postal Reform in the 115th Congress – H.R. 756, the Postal Service Reform Act of 2017,” February 7, 2017.

[6] U.S. Military Retirement Fund Audited Financial Report 2015, page 17.

[7] Center for Retirement Research, “State and Local Pension Brief 50, The Funding of State and Local Pensions: 2015-2020,” June 2016.

[8] Standard & Poor’s RatingsDirect: “U.S. State Pensions: Weak Market Returns Will Contribute To Rise In Expense,” September 12, 2016.

[9] S&P Global Ratings, “U.S. State Ratings Methodology,” October 17, 2016, page 21.

Retiree Healthcare

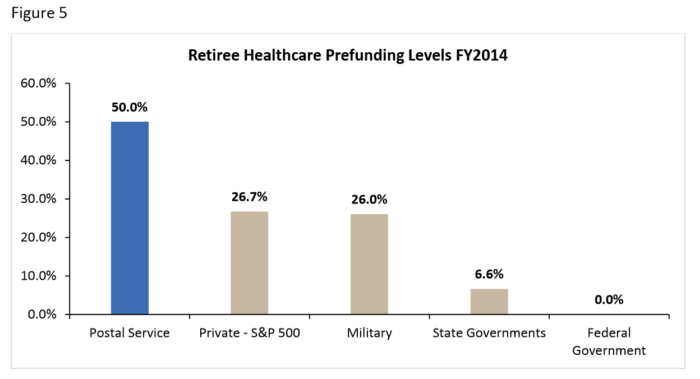

The Postal Service has also prefunded its retiree healthcare liabilities at a much higher level than the federal government, most state and local governments, and those major private corporations that still offer such benefits, as summarized in Figure 5:

- The federal government has not pre-funded any retiree healthcare obligations for civilian workers.[10]

- The Department of Defense has funded more than half of the liability for Medicare-eligible retirees, but has not funded any retiree healthcare obligations for pre-Medicare eligible retirees. The overall funded ratio for its plans was 26.0% for FY2014. [11]

- A majority of 56% of the 264 S&P 500 companies that still offered post-employment medical benefits in FY2014 had not pre-funded any obligations. In the aggregate, these 264 companies had a 26.7% funded level. [12] Across the private sector, there is no equivalent statute to the Public Protection Act of 2006 addressing retiree healthcare liabilities or funding requirements.

- The average and median funded level for state governments was also 0% in FY14 – the typical state government had not pre-funded any liabilities. In aggregate, state governments had a 6.6% funded level for retiree healthcare in FY2014. Similarly, a review of state and local retiree healthcare prefunding using FY2013 data by the Center for Retirement Research at Boston College that included roughly 750 local government and school district entities indicated an aggregate nation-wide funded level of 7% for those entities and the 50 states. [13]

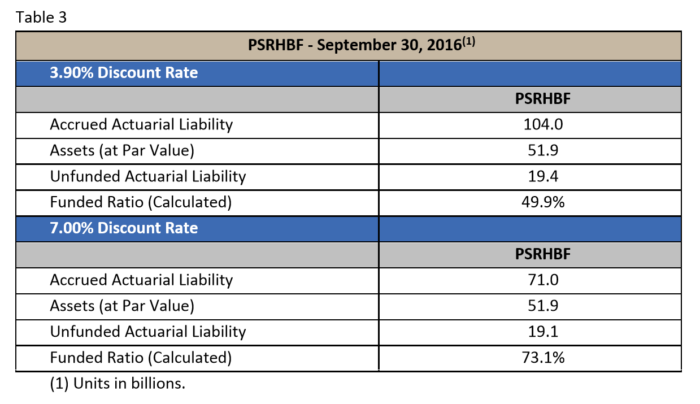

The USPS retiree healthcare funded ratio of 50.0% for FY2014 was primarily used above because that is the most recent year for which comparative information is broadly available. More recent financial statements report that this ratio dipped to 47.9% as of FY2015 but is estimated to improve to 49.9% in FY2016 based on continued asset growth and a $1.2 billion reduction in the estimated liability. Although full funding remains an appropriate long-term goal, the Postal Service, again, continues to be far better funded than most public employers along this path.

While state and local governments have a relatively long tradition of prefunding pensions actuarially, the vast majority of state and local governments have viewed and funded retiree healthcare benefits on a pay-as-you-go basis until much more recently. In 2004, Governmental Accounting Standards Board (GASB) Statement 45 was issued requiring the reporting of Other Post-Employment Benefit (“OPEB”) plans on an actuarial basis. While many governments continue to use a pay-as-you-go approach or prefund at far below actuarially determined levels, GASB 45 did change awareness of these liabilities. In turn, this has led to the establishment of more dedicated trusts for pre-funding the benefit, as well as increased long-term planning to address (and, in many cases, reduce) the benefit structures.[14] Nonetheless, this relatively recent increase in focus on retiree healthcare means that full actuarial funding remains a long-term, multi-decade challenge for most state and local governments providing such benefits.

In this context – within which most comparable organizations are not yet even making full actuarial contributions toward retiree healthcare obligations – the PAEA required a fixed schedule of USPS annual contributions into the Postal Service Retiree Health Benefits Fund (PSRHBF) from FY2007 through F2016 that was actually substantially greater than an actuarially determined approach. [15]In several GAO reports, these amounts have been described as “significantly frontloaded.”[16] Further, through FY2016, the PAEA schedule also required the USPS to contribute the full prefunding contribution and to continue to pay the cost of the benefits separately out of operations. Starting in FY2017, the USPS can now pay current retirees from the PSRHBF, such that the net fiscal impact on the operating budget is reduced by the pay-as-you-go obligations – an approach much more consistent with standard practice for other public and private sector retirement plans.

Absent these extraordinary retiree healthcare funding requirements in place through FY2016, the USPS would not have recorded the net losses from operations shown in recent years, and would not be reporting a $33.9 billion liability associated with “defaulted” payments. In other words, using the same retiree healthcare funding approaches adopted by the federal government generally, as well as by most state and local governments, the Postal Service “financial crisis” would substantially fade away.

Longer term, there are, of course, worthwhile benefits to prefunding retiree healthcare under a sound funding policy and as part of a broader total compensation strategy. Such an approach can help to fully and appropriately address the cost of such liabilities over time, more equitably allocate costs across generations, and better position an organization financially for the decades ahead. This long-term challenge, however, is distinct from an immediate crisis – and this goal can be achieved without a massive increase in revenue requirements.

[10] Statement of Postmaster General and CEO Megan J Brennan before the House Oversight and Government Reform Committee Hearing “Accomplishing Postal Reform in the 115th Congress – H.R. 756, the Postal Service Reform Act of 2017,” February 7, 2017; Financial Report of the U.S. Government, 2014.

[11] U.S. Department of Defense, Agency Financial Report, Fiscal Year 2015, page 88.

[12] Standard & Poor’s RatingsDirect: Pensions and OPEBs are Heading into the Sunset, A HalfTrillion Dollars Short, June 17, 2015.

[13] Center for Retirement Research, “How Big a Burden Are State and Local OPEB Benefits?, State and Local Project Brief 48,” March 2016, page 4

[14] Center for State and Local Government Excellence, “Prefunding Other Post-Employment Benefits in State and Local Government,” September 2009; National Association of State Retirement Administrators, “Spotlight on Retiree Health Care Benefits for State and Local Employees in 2014,” December 2014.

[15] PL 109-435, Postal Accountability and Enhancement Act, December 20, 2006.

[16] GAO-17-404T, “USPS Key Considerations for Restoring Fiscal Sustainability,” February 7, 2017; GAO-13-112, “USPS Status, Financial Outlook, and Alternative Approaches to Fund Retiree Health Benefits,” December 2012.

IV. Nominal USPS Funded Ratios are Based on Conservative Assumptions and Practices

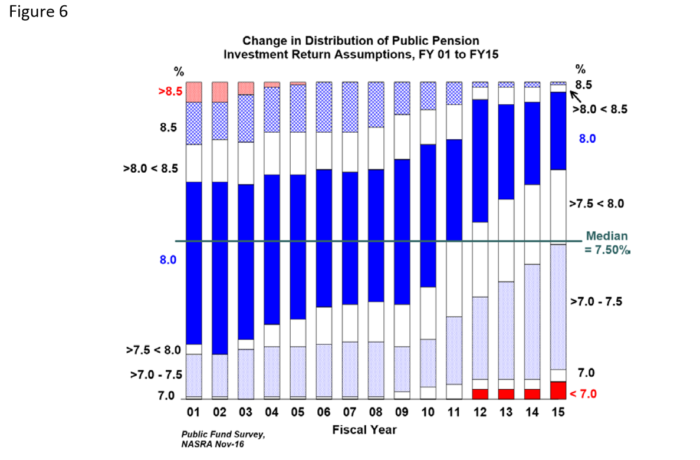

In addition to the relative strength of Postal Service retiree benefit funding when funded ratios are compared on a nominal basis, it is important to note that retirement plans report such ratios based on varying actuarial assumptions that can impact the scale of the calculated liability and funded status. As noted in the most recent Public Fund Survey[17] conducted by the National Association of State Retirement Administrators:

Of all actuarial assumptions, a public pension plan’s investment return assumption has the greatest effect on the projected long-term cost of the plan. This is because over time, a majority of revenues of a typical public pension fund come from investment earnings. Even a small change in a plan’s investment return assumption can impose a disproportionate impact on a plan’s funding level and cost.

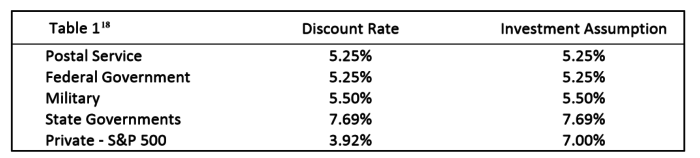

In this regard, the assumed rates of investment return and associated discount rates applied to liabilities for the USPS, civilian Federal Government, and Military plans are all significantly lower than those used for almost all state and local pensions. This difference increases the reported size of the calculated USPS unfunded liability relative to these non-federal plans. [18]

Figure 6 below, drawn directly from the November 2016 Public Fund Survey summary report, further illustrates the range of investment return assumptions across the full Survey dataset for FY2015. This Survey contains data on public retirement systems estimated to comprise approximately 85% percent of the state and local government retirement system community, compiled primarily by the Center for Retirement Research at Boston College, based largely on annual financial reports. As may be noted, there has been a clear trend toward more conservative investment return assumptions in the recent economic environment, however, the significant majority of systems continue to assume 7.0% or more for their returns.

One of the primary reasons for the lower investment return assumptions in the federal-related plans is that such plans are generally more restricted in their investment options. This dampens the potential USPS investment returns relative to all other public and private pension plans. As a result, the lower projected returns increase the reported size of the unfunded liability relative to state and local pension plans.

As detailed in the subsequent Section V of this report, a modification of these restrictions could potentially achieve greater long-term returns and result in a lower reported liability. From the perspective of mainstream practice across the state and local government sector, the federal investment constraints are extraordinary – and it is remarkable that the Postal Service has been able to achieve the comparatively high funded levels it has reached despite such limited investment options. Viewed in household terms, this would be akin to investing all of one’s 401(k) retirement assets in a money market account.

At the same time, it may also be noted that, because the current USPS and federal approach carries less investment risk than typical state and local plans, the likelihood of meeting reported actuarial assumptions is higher. In turn, this implies that the USPS faces less risk of future shortfalls emerging based on actual investment returns falling short of plan assumptions.

To further illustrate the impact of these varying investment return assumptions, we calculated the estimated [19] USPS funded ratios assuming discount rates of 7.0%, consistent with the average assumption for S&P 500 plans in FY2014, and at the comparatively conservative end of the range for state and local government pension plans.

With a 7% discount rate assumption, as shown in Table 2, the USPS plans would be 114.6% funded. Similarly, as shown in Table 3, the PSRHBF funded ratio would also improve under higher discount rate assumptions, rising to 73.1% with a 7.0% rate.

In the aggregate, with a 7.0% discount rate, the reported overfunding in the pension plans would exceed the remaining retiree healthcare liability, such that the total assets of nearly $335 billion across all three plans would exceed the combined actuarial liability of $318 billion – for a funded ratio above 100%.

In addition to low investment return and discount rate assumptions, Postal Service retirement system actuarial reports and funding requirements are also based on salary growth and demographic assumptions developed by the federal Office of Personnel Management (“OPM”) using government-wide data, rather than USPS-specific demographics and assumptions. Actuarial analysis commissioned by the Postal Service indicates that the OPM methodology results in higher liabilities and funding requirements than a USPS-specific calculate would yield:

“OPM calculated that our portion of the FERS plan was underfunded by $3.6 billion as of September 30, 2014. We continue to request that OPM reconsider its use of such government-wide factors and instead apply Postal Service-specific economic and demographic assumptions, which we believe would have resulted in a surplus of approximately $1.2 billion as of September 20, 2014, the most recent period in which such comparisons have been calculated.” [20]

Across all of the USPS retirement programs (FERS and retiree healthcare, in addition to CSRS), the OIG has estimated that use of Postal Service-specific assumptions would have generated a potential net reduction in liabilities of $8.5 billion as of FY2012, subject to annual fluctuation since. [21]

[17] National Association of State Retirement Administrators, “Public Fund Survey, Summary of Findings for FY2015,” December 2016.

[18] Sources: USPS Report on Form 10-K, Civil Service Retirement and Disability Fund 2015 Annual Report, U.S. Military Retirement Fund Audited Financial Report 2015, NASRA Issue Brief: Public Pension Plan Investment Return Assumptions, 2015, Standard & Poor’s RatingsDirect: Pensions and OPEBs are Heading Into The Sunset, A Half-Trillion Dollars Short, June 17, 2015.

[19] For this analysis, we used a methodology consistent with that used by the credit rating agency, Moody’s Investors Service, for normalizing liability estimates across plans. Moody’s Investors Service, Cross Sector Rating Methodology, “Adjustments to US State and Local Government Reported Pension Data,” April 17, 2013. An actuarial analysis would reflect the unique benefit structure and demographics that affect the time-weighted profile, or duration, of future benefit payment liabilities. Because such durations are not generally reported, Moody’s uses a common assumption of 13 years, which is based on durations calculated from a sample of public plans. In turn, this duration assumption is used to implement the discount rate adjustment. A plan’s reported accrued liability is projected forward for 13 years at the plan’s discount rate, then discounted back at the high-grade bond index rate. For our adjustments to Postal Service data, we similarly assumed a 13 year duration, projected the liability forward at the plan assumed rates, and discounted back at 7.0%.

[20] USPS 2016 Report on Form 10-K, page 23.

[21] USPS OIG Report FT-WP-15-003, “Considerations in Structuring Estimated Liabilities,” January 23, 2015; FT-MA-13-022, “Using USPS – Specific Assumptions for Calculating the Retiree Health Care Liability,” September 27, 2013; FT-MA-13-024, “Using USPS – Specific Assumptions for Calculating the Federal Employees Retirement System Liability,” September 27, 2013; and FTMA-13-023, “Using USPS – Specific Assumptions for Calculating the Civil Service Retirement System Liability,” September 27, 2013.

V. Reasonable Opportunities are Available to Reduce These Liabilities

Over the long-term, funding retiree benefits at 100% levels using reasonable actuarial assumptions is an appropriate goal. At the same time – due to factors such as evolving longevity expectations as lifespans have tended to grow longer, market underperformance during the 2000- 2010 decade, and the relatively short period of time since new accounting standards sharpened focus on the value of prefunding retiree healthcare – very few U.S. retirement plan sponsors are currently meeting this standard.

As a result, improving funded status is widely understood to often require a long-term, multi-decade funding approach. In addition, comprehensive retiree liability management should also include focus on capturing opportunities to reduce risk and cost exposure, rather than exclusively relying on increased funding.

In this regard, the Postal Service has advocated for several statutory reforms that would potentially provide financial relief from retiree benefit liabilities, and substantially, if not completely, resolve the current USPS unfunded liabilities.

One approach currently under Congressional consideration is encapsulated in H.R. 756, the Postal Service Reform Act of 2017. The proposed Act would authorize USPS to obtain its own medical insurance rating based on its own demographic pool and experience, would require full retiree medical insurance integration with Medicare, and would require OPM to value the USPS pension and OPEB liabilities based on the specific demographics and experience of USPS. [22]

The Postmaster General’s testimony on H.R. 756 [23] estimates a total reduction in the liability of $54 billion from Medicare integration alone, substantially eliminating the USPS unfunded retiree healthcare liability and any associated ongoing payments to amortize this obligation. In addition, this reform would also reduce the estimated ongoing normal costs for current service. Nationally, such Medicare integration is the standard practice across the state and local government sector and among large private companies that still offer retiree healthcare. For decades, the Postal Service and its employees have contributed into the Medicare system through payroll taxes, and it is reasonable for these integrated benefits to be received in return. Medicare integration would place the Postal Service on equal footing with its private sector competitors, eliminating what is now effectively a ratepayer subsidy for the overall Medicare system.

H.R. 756 would also direct OPM to prepare USPS actuarial valuations and estimates for pension and OPEB estimates using specific USPS demographics, workforce trends, and experience. As noted elsewhere in this report, this is another change that has been suggested numerous times by GAO and the USPS OIG, estimated by the OIG to potentially generate a net reduction in liabilities of $8.5 billion. [24]

As also referenced elsewhere in this report, the assets held in trust by the Treasury for CSRS, FERS, and PSRHBF are by law invested conservatively in special issue Treasuries restricted to maturities of 15 years or less. [25] While this requirement does provide stability and protection from risk and volatility, the conservative asset class and duration of the investments significantly lowers the discount rate used for pension assets compared to other public and private plans, which typically incorporate diversification in assets such as high-grade corporate bonds and equities.

Allowing diversification into higher-yield asset classes with longer duration would potentially increase long-term returns on the assets while also allowing OPM to appropriately apply a higher discount rate for valuation purposes, a change that would reduce the size of the reported unfunded liability. Legislation has been introduced to permit some diversification beginning with the USPS OPEB liability assets held in the PSRHBF, through H.R. 5707 in the previous 2015-2016 session of Congress, and H.R. 760 in the new 2017-2018 session. This legislation would allow up to 25-30 percent of the PSRHBF to be invested in index funds with an allocation patterned after the longest-duration target fund provided in the federal Thrift Savings Plan (“TSP”). [26] Compared to typical practice across the state and local government sector, this would continue to be an extraordinarily conservative investment approach.

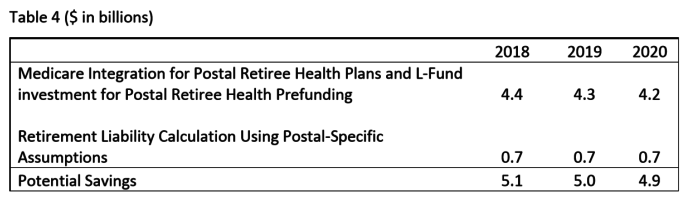

The annualized savings estimated by the USPS [27] from its full set of proposed reforms, which include Medicare integration for retiree healthcare, use of Postal-specific actuarial assumptions for all retiree benefits, and flexibility to invest for retiree healthcare prefunding consistent with the longest duration “L” fund in the Thrift Savings Program, are included in Table 4 below. Note that any additional potential savings from even greater flexibility for pension investments and/or restructuring of benefit plan design are not assumed in Table 4.

It may also be noted that these potential savings as outlined in Table 4 would be over and above the approximately $4 billion per year in annual savings already being experienced beginning in FY2017 under existing law based on the shift to an actuarial basis for retiree healthcare prefunding (with current retiree benefit payments made from the trust), rather than continuing the PAEA schedule of frontloaded, fixed payments. [28]

[22] H.R. 756 (2017-2018); Statement of the Postmaster General before the House Oversight and Government Reform Committee Hearing, U.S. House of Representatives, February 7, 2017.

[23] Written Testimony of the Postmaster General before the House Oversight and Government Reform Committee Hearing, May 11, 2016, page 14. The Postmaster General cites this $54 billion savings as eliminating 94% of the associated unfunded liability. It may be noted, however, that the USPS 2016 Report on Form 10-K, page 27, cites the total estimated retiree healthcare liability as of September 30, 2016 to be $52.1 billion.

[24] USPS OIG Report FT-WP-15-003, “Considerations in Structuring Estimated Liabilities,” January 23, 2016; FT-MA-022, “Using USPS Assumptions for Calculating the Retiree Health Care Liability,” September 27, 2013; FT-MA-13-023, “Using USPS Specific Assumptions for Calculating the Civil Service Retirement System Liability,” September 27, 2013.

[25] U.S. Office of Personnel Management Civil Service Retirement and Disability Fund Annual Report, Fiscal Year Ended September 30, 2015; 2016 Report on Form 10-K.

[26] House Report 114-859 on H.R. 5707

[27] Written Testimony of the Postmaster General before the House Oversight and Government Reform Committee Hearing, May 11, 2016, page 16.

[28] United States Postal Service 2016 Report on Form 10-K, page 28.

VI. With Over $338 Billion in Retiree Benefit Prefunding Assets Already On Hand, Even Without Reform, the USPS is Not Projected to Face Budget Pressure From Payment Obligations for Many Years

As of September 30, 2016, the USPS reported $286.5 billion in pension plan assets and $51.9 billion in retiree healthcare prefunding, for total assets of nearly $338.4 billion. These resources provide significant funding capacity for an extended period that allows the Postal Service time to pursue the available reform opportunities that would reduce its long-term funding pressures without major rate increases.

To illustrate this capacity, the following analysis estimates the level of these assets remaining as of September 30, 2027 – just over ten years from now – assuming that the full benefit payment streams to USPS retirees are funded solely from the prefunded assets on hand as of September 30, 2016, with no additional contributions into these retirement funds. For this estimate, the following assumptions are used:

- Benefit payment streams are based on management projections for FY2017-FY2021 as included in the USPS financial statements.[29] For FY2022 through FY2027, we assume that the projected FY2021 payments would further increase each year thereafter by the average cost growth rate for the first five-year period. For retiree healthcare, note that this approach is more conservative than the USPS actuarial valuation assumption of declining medical inflation.

- Assets in the funds are assumed to earn interest consistent with the current federal actuarial assumptions and highly conservative investment practices (5.25% for pensions, 3.9% for retiree healthcare). All benefits are assumed to be paid from assets in the funds with no additional contributions or pay-as-you-go funding made by the USPS.

With the above assumptions, in just over ten years, as of September 30, 2027:

- There would still be over $111.0 billion in the CRS for Postal Service employees.

- There would still be nearly $122.5 billion in FERS for Postal Service employees.

- There would still be over $9.8 billion in the PSRHBF.

In the aggregate, at the end of the ten-year period ahead, these three Postal Service retirement funds would be projected to have nearly $243.3 billion in prefunding still available for retiree benefits – again, even with no additional employer contributions, no reform of investment practices, no Medicare integration, and no use of Postal-service specific actuarial assumptions. Although the above projections should not be interpreted as a recommendation for the Postal Service to cease prefunding of its retirement liabilities, this analysis does illustrate that these funding challenges are multi-decade in nature rather than reflective of any immediate crisis. Sustainability can be responsibly addressed over time, without requiring precipitous increases to funding, potentially in conjunction with reasonable policy reforms that further reduce funding pressures.

[29] United States Postal Service, 2016 Report on Form 10-K, pages 25, 28.

VII. Other Balance Sheet Assets are Growing in Value and Stronger than They Appear in the Postal Service Financial Statements

The condition of the Postal Service balance sheet is not just a function of the scale of USPS liabilities. A full evaluation should also assess the value of the assets available to offset such liabilities.

As of the end of FY2016, the USPS reported nearly $8.1 billion in Cash and Cash Equivalents as assets in its financial statements, [30] a line item that has grown steadily in recent years from $2.1 billion as of FY2012.

In addition, as of FY2016, the Postal Service reported $15.3 billion in Property and Equipment, Net as assets in its financial statements. While this amount appears to have been reported consistently with Generally Accepted Accounting Principles (GAAP), past analyses have indicated that the market value for these assets – primarily real estate – is many times higher.

Pursuant to accounting treatment, real estate assets are recorded at cost, inclusive of interest for any capital borrowing, less allowances for depreciation and amortization. For depreciation, estimated useful lives are used that range from 3 to 40 years based on asset class under the straight-line method. This accounting approach can be referred to as “net book value.” Alternatively, property and equipment – the majority of which is comprised of building, land, and leasehold improvements, with other categories including equipment and vehicles – can be viewed from a “fair market value.”

Past OIG reports indicate that the fair market value for the Postal Service real estate holdings would be far higher than the net book value shown in the financial statements. In a 2011 study, for example, the National Postal Museum property was found to have had a purchase price of $47 million and an assessed tax value of $304 million. [31] While this particular property may not be representative of all USPS real estate, the OIG developed an estimate of aggregate real estate value of $85 billion based on long-term commercial real estate trends in a subsequent 2012 analysis [32] – more than six times the net book value of land and buildings.

Even at the 2012 estimated real estate value, the USPS fair market value would be approximately $70 billion above the net book value for all property and equipment reported on the Postal Service balance sheet. Further, since this 2012 estimate was developed, U.S. commercial real estate prices have averaged more than double digit growth annually, increasing by 40.0% overall from Q4 2012 to Q4 2015 alone. [33]Applying these growth rate factors to the 2012 OIG estimate indicates potential 2015 Postal Service real estate fair market value of $119 million – over $100 million more than the reported net book value.

When addressing such Postal Service real estate assets, the OIG has noted:

“Any discussion of unfunded liabilities should take into consideration assets that could be used to satisfy the liabilities.” [34]

In public sector finance, there are often significant variances between accounting treatments and the numbers used for budgeting and other financial planning. In the case of real estate assets, for example, there may be the potential for future sale or sale/leaseback opportunities, and such transactions and any resulting proceeds would have returns driven by fair market value, not net book value. Accordingly, the more relevant perspective for taking these assets into account for financial analysis is the fair market value, not the GAAP net book value.

While Postal Service management has responded accurately to past OIG reports that such assets are often not immediately available to liquidate or pledge directly against retiree benefit liabilities, the true value of these assets is nonetheless quite relevant when evaluating long-term balance sheet condition. In the near-term and intermediate term, as the Postal Service itself has also noted, assets in excess of needs can be identified to obtain best value from lease or sale. [35] In other cases, strategies might be developed to relocate certain USPS operations to lower cost locations while monetizing the value of current, high value real estate. Perhaps most significant, in the event of a more severe technological or other long-term business disruption to the existing Postal Service business model somewhere in the decades far ahead, an even greater percentage of the significant fair market value of these real estate assets would become available to address any ongoing, unfunded obligations.

This fair market value represents an important safety net for the overall sustainability of the Postal Service’s long-term finances, and, again, should be considered when evaluating this fiscal position. Further, to the extent that current fair market value has only been estimated, a more thorough review and valuation would be an important area for future study to accurately determine overall Postal Service financial condition going forward.

[30] 2016 Report on Form 10-K, page 12.

[31] USPS OIG, FF-MA-11-118, “Management Advisory – Leveraging Assets to Address Financial Obligations,” July 12, 2011.

[32] USPS OIG FT-MA-12-002, Pension and Retiree Health Care Funding Levels,” June 18, 2012.

[33] International Monetary Fund, Commercial Real Estate Prices for United States© [COMREPUSQ159N], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/COMREPUSQ159N, March 2, 2017

[34] USPS OIG FT-WP-15-003, “Considerations in Structuring Estimated Liabilities,” January 23, 2015.

[35] USPS OIG FT-MA-12-002, “Pension and Retiree Health Care Funding Levels,” June 18, 2012

IIX. USPS Total Compensation Premium

Multiple past analyses have well-documented the substantial and longstanding compensation premium paid to USPS employees above the levels prevalent among comparable private sector workers. The 2003 Report of the President’s Commission on the United States Postal Service, for example, found that:

“Postal Service workers currently enjoy the best of both the public- and private-sector worlds – salaries akin to those offered by leading corporations, plus the substantial job security and benefits associated with Federal employment.” [36]

In testimony submitted to the 2003 Presidential Commission, Dr. Michael Wachter of the University of Pennsylvania outlined the long history of this comparability advantage, detailing his findings of a significant “wage and benefit premium” for Postal Service workers based on his detailed economic research, comparison of wages and benefits to private sector datasets, and extraordinarily low turnover. Dr. Wachter is a prominent cross-disciplinary scholar in the fields of law and economics, who has held full professorships in Economics, Management, and Law and Economics at the University of Pennsylvania’s School of Arts and Sciences, Wharton School, and Law School respectively. As a labor economist, Dr. Wachter had been engaged by the Postal Service since 1981 as a compensation analyst and expert for employee interest arbitration.

Also in Dr. Wachter’s testimony before the 2003 Presidential Commission, he cited multiple neutral arbitrators dating back to the early 1980’s who have also independently found that a postal wage and benefit premium exists. For example, in a 2002 interest arbitration award between the Postal Service and the American Postal Workers Union (“APWU”), the neutral arbitration panel chair wrote

In concluding that there exists a Postal Service wage premium, I join a long list of arbitrators who have reached the same conclusion.”[37]

Further, these arbitral findings of a wage premium continue through the most recent Postal Service proceedings. In a July 2016 APWU award, for example, the neutral panel chair wrote:

“In weighing the parties’ arguments on wage and benefit comparability, certain factors stand out. Initially, I am persuaded, as the Postal Service asserts, that the package of economic benefits received by bargaining unit employees – retirement benefits, retiree health care, paid leave, low employee health care contributions, and a no-layoff provision – are superior to those typically available to private sector employees. Another factor which stands out are the quit rate data, which show that career Postal Service employees voluntarily leave their jobs at a rate far lower than do private sector employees. Despite APWU arguments to the contrary, I consider this as powerful evidence that APWU-represented employees consider their jobs with the Postal Service to be superior to the alternatives available to them elsewhere.”[38]

For this report, we have updated these past analyses with several new and independent perspectives. The first of these new approaches compares cash compensation data developed by the BLS for three major Postal Service occupations relative to pay rates for comparable occupations in the broader labor market. These data are drawn from the BLS Occupational Employment Statistics (“OES”) program, the most comprehensive source of regularly produced occupational employment and wage rate information for the U.S. economy. The OES program surveys approximately 1.2 million nonfarm establishments to produce employment and wage estimates for about 800 occupations. The OES program produces these occupational estimates for the nation as a whole and varying geographic areas, and by ownership or industry corresponding to the North American Industry Classification System (“NAICS”) industrial groups. Wage estimates for the OES survey represent straight-time, gross pay, exclusive of premium pay – so does not include all forms of cash compensation such as shift differentials and overtime also earned by many USPS workers.[39]

Under the OES program, the three occupational categories specific and exclusive to the Postal Service are noted below, all falling within the broader BLS grouping of Postal Service Workers (43-5050): 43-5051 – Postal Service Clerks; 43-5052 – Postal Service Mail Carriers; and, 43-5053 – Postal Service Mail Sorters, Processors, and Processing Machine Operators.

In the tables that follow, OES median wages are presented for these three Postal Service occupations[40] relative to the median wages for comparable private sector occupations nationally as of the most recent reference period of May 2015. To determine comparable private sector occupations, the O*Net OnLine database sponsored by the U.S Department of Labor was first used to identify occupations characterized as “related” based on similar job qualifications and characteristics.[41] O*Net typically identifies ten (10) occupations to be related. In turn, two of these related occupations were selected for each Postal Service category based on a particularly high degree of comparability, and included in the tables below. In addition to this BLS data, the pay scale ranges for common Postal Service pay grades within these categories – in both career and non-career positions – are shown in the bottom segment of each table.

[36] Report on the President’s Commission (2003), page 117.

[37] President’s Commission of the USPS, Statement of Michael L. Wachter, April 29, 2003, page 14.

[38] United States Postal Service and American Postal Workers Union, AFL-CIO, Interest Arbitration Decision and Award, Effective Date: July 8, 2016, page 11. Other analysts of the Postal Service’s finances have also reached similar conclusions. In 2007, for example, the Federal Trade Commission similarly found that “Postal Service labor costs tend to be higher than private counterparts.” (Federal Trade Commission, Accounting for Laws that Apply Differently to the United States Postal Service and its Private Competitors, December 2007, page 37).

[39] Bureau of Labor Statistics, U.S. Department of Labor, Occupational Employment Statistics [www.bls.gov/oes/].

[40] To validate the OES data, average (mean) hourly earnings were calculated from the National Payroll Summary of the U.S Postal Service for FY2015 pay period 11, which generally aligns with the most recent OES reference period. To align with the OES data that aggregates both career and non-career service Postal Service workers, full-time and part-time, in some cases spanning different bargaining units (e.g., City and Rural Letter Carriers), National Payroll Summary earnings and hours were similarly grouped. Although survey methodology and workforce fluctuations do cause some minor variances across these datasets, the overall averages (means) from OES and the averages calculated from the National Payroll Summary varied by less than 5.0% for all three job categories and by less than 1.0% for two of the three occupations. This congruence indicates a high degree of reliability for the OES results.

[41] O*NET OnLine. National Center for O*NET Development, n.d. Web. 20 Feb. 2017. https://www.onetonline.org/>.

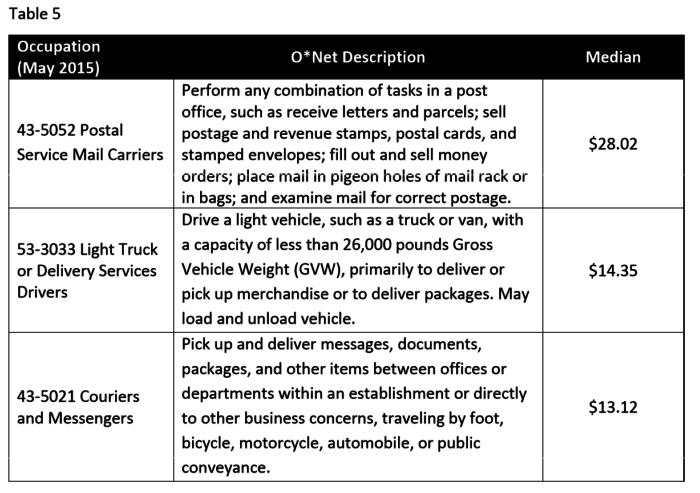

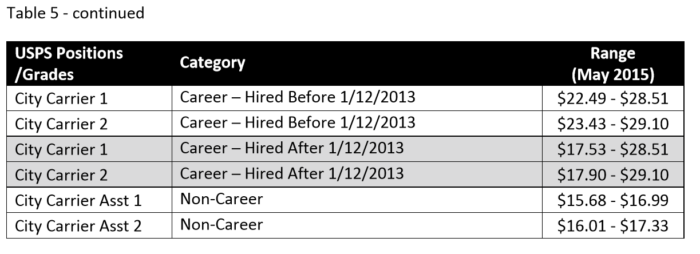

Mail Carriers

As shown in Table 5, the Postal Service Mail Carrier wage premium at median over these comparable private sector occupations was 95.3% above Light Truck or Delivery Services Drivers and 115.0% above Couriers and Messengers.

Of note, the Postal Service Tier 2 rate for City Carrier Assistants in effect as of May 2015 ranged from $15.68 to $17.33 per hour, depending on step and grade – a level more closely aligned with the market rates for comparable work in private industry. Including subsequent pay increases, the USPS Tier 2 rate for City Carrier Assistants in effect as of February 2016 ranges from $16.06 to $17.74.

Among the other private sector occupations identified by O*Net as related but not charted above, median pay ranged from $10.11 to $14.25 per hour. In all cases, Postal Service workers maintained a significant wage premium, with comparable general labor market pay more consistent with the Postal Service Tier 2 rates.

Mail Handlers

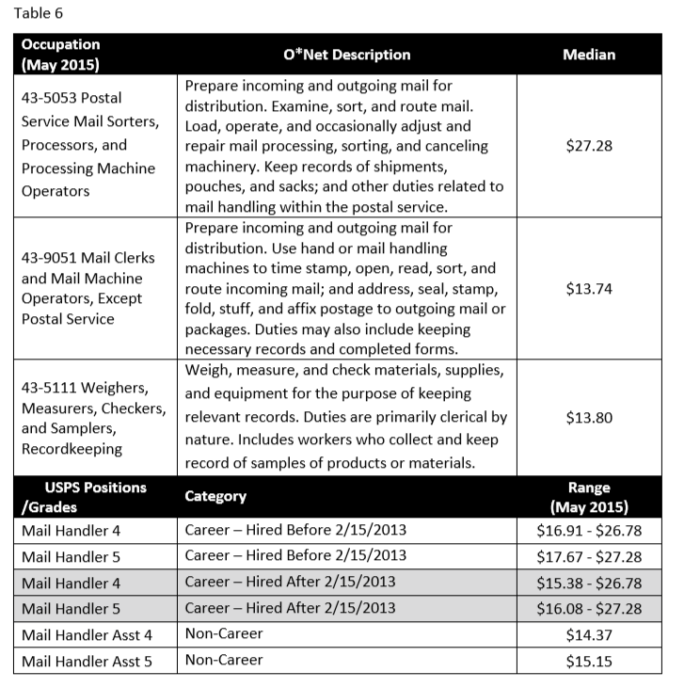

As detailed in Table 6 that follows, the Postal Service Mail Handler wage premium at median over comparable private sector occupations was 98.5% above Mail Clerks and Mail Machine Operators, Except Postal Service and 97.7% above Weighers, Measurers, Checkers, and Samplers, Recordkeeping.

Of note, the Postal Service Tier 2 rate for Mail Handler Assistants in effect as of May 2015 ranged from $14.37 to $15.15 per hour, depending on step and grade – a level more closely aligned with the market rates in private industry. Including subsequent pay increases, the current Postal Service Tier 2 rate for City Carrier Assistants in effect since November 2016 ranges from $15.12 to $15.94.

Among additional private sector occupations identified by O*Net as related but not charted below, median pay ranged from $10.01 to $15.26 per hour. In all cases, Postal Service workers maintained a significant wage premium, with comparable general labor market pay more consistent with the Postal Service Tier 2 rates.

Postal Clerks

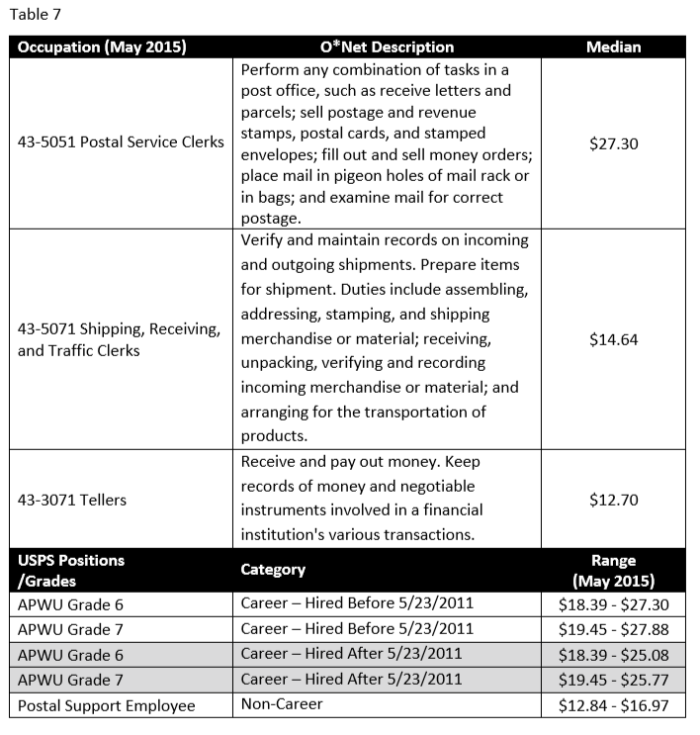

For Postal Service Postal Clerks, as shown in Table 7, the wage premium at median over comparable private sector occupations was 86.5% above Shipping, Receiving, and Traffic Clerks and 115.0% above Tellers.

Of note, the Postal Service Tier 2 rate for Postal Support Employees in effect as of May 2015 ranged from $12.84 to $16.97 per hour, depending on step and grade – a level more closely aligned with the market rates for comparable work in private industry. Including subsequent pay increases, the current Postal Service Tier 2 rate for Postal Support Employees in effect as of November 2016 ranges from $13.51 to $17.82. Similarly, among the other private sector O*Net-identified related occupations, median pay ranged from $10.11 to $14.25 per hour. In all cases, Postal Service workers maintained a significant wage premium, with comparable general labor market pay more consistent with the Postal Service Tier 2 rates.

In past arbitrations, Postal Service unions have argued that the wage premium documented above is not present or as pronounced when measured against other selected industries, such as uniformed service delivery competitors for letter carriers or the telecommunications and airline industries for clerks.[42] Certainly, in any comparison of occupational pay, some industries will tend to pay more or less than others in wages. Such industry variations may be based on competitive pressures (or weakness of such pressures in a regulated industry), primary geographic location, unionization, differences in approach to benefits, historical evolution of that industry, and a broad range of other factors.

In practice, however, the Postal Service competes in the general labor market – not against just a handful of industries hand-selected by the unions for comparison. The pay comparability statute reflects that: compensation and benefits or postal employees should be comparable to the “compensation and benefits paid for comparable levels of work in the private sector of the economy”[43] not comparability with a limited subset of the private sector carved out based on isolated factors. By looking at wages for similar occupations across all U.S. private industry, our analysis comports more closely with this federal policy, as the job qualifications and characteristics of the related occupations identified by O*Net align well with the “levels of work” in the USPS categories.

Further, our comparison aligns with the full labor market within which the Postal Service recruits and retains. In this context, both the almost nonexistent quit rates for career USPS positions, and the Postal Service’s ability to routinely fill non-career positions at lower Tier 2 rates despite the lack of job security, undesirable schedules, and limited benefits all indicate that true market wages and benefits for comparable levels of work are well below those of Postal Service career positions – and well below those of any other anomalous employers with compensation approaching such levels.

[42] See, for example NALC 2013 arbitration award page 7, and APWU 2016 arbitration award, page 10.

[43] 39 U.S.C. §1003(a) (39 U.S.C. § 101(c) is to the same effect).

IX. USPS Benefits Premium

In addition to a substantial wage premium, Postal Service workers receive exceptionally generous benefits as a further component of total compensation. In some notable cases, these benefits are currently determined by federal statute – including pension benefits, participation in the federal employee health benefits system, and retiree healthcare coverage. In other cases, such as paid leave and active employee healthcare premium contributions, Postal Worker benefits are – or can be – determined primarily through collective bargaining. In both cases, the high value of Postal Service benefits adds to the overall total compensation premium above comparable private sector norms.

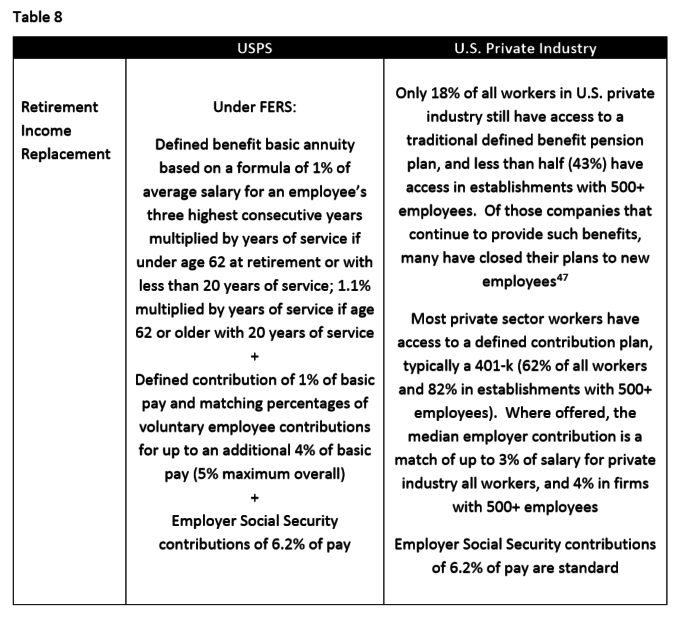

Postal Service Retirement Benefits

Postal Service employees hired since 1987 participate in FERS, which provides both a defined benefit basic annuity and a defined contribution TSP component, in addition to Social Security coverage. This FERS program can be characterized as a “hybrid” retirement plan that combines both defined benefit and defined contribution features.[44]

In comparison, as outlined in the table that follows drawing on data from the BLS National Compensation Survey as of March 2016, most private sector employees now receive only a 401(k)-style defined contribution benefit, which typically has a lower cost and less risk for the employer, and less replacement income and retirement security for participating employees. As the OIG found in a 2014 white paper on retirement benefits:

“Private company and public sector retirement plans have undergone significant changes over the past 20 to 30 years. Pension plans used to be the most common form of retirement plan in the U.S., but recently 401 (k) plans have become more popular. Benchmarked organizations are phasing out costly pension programs and implementing 401 (k) matching programs.”[45]

In FY2016, based on analysis of the Postal Service National Payroll Summary, the USPS contributed approximately $3.73 per employee hour worked toward retirement benefits, excluding Social Security and retiree healthcare. In contrast, the typical contribution in private industry was just $1.25 per hour worked according to the BLS Employer Costs for Employee Compensation (“ECEC”) report.[46]

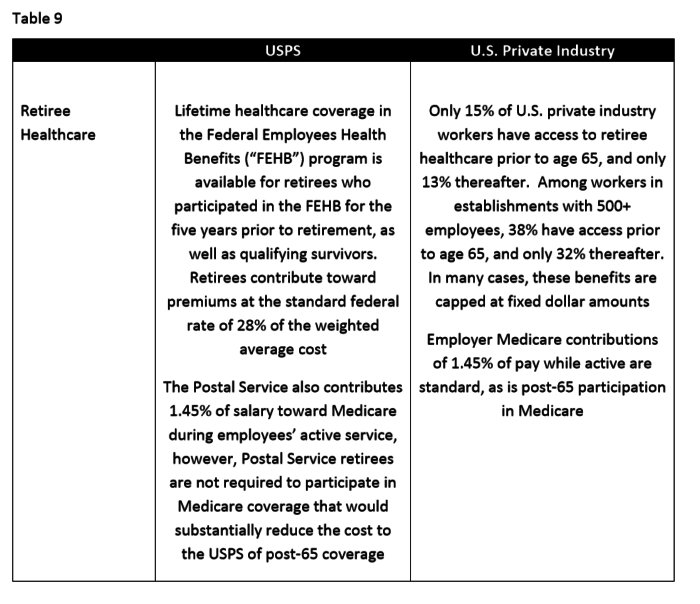

In addition, the USPS provides retiree lifetime healthcare coverage in the Federal Employees Health Benefits (“FEHB”) program for former employees who participated in the FEHB for the five years prior to retirement, as well as qualifying survivors. Retirees contribute toward premiums at the standard federal rate of 28% of the weighted average cost. In contrast, retiree healthcare has become increasingly rare in the private sector. Again according to the March 2016 BLS National Compensation Survey, only 15% of U.S. private industry workers have access to retiree healthcare prior to age 65, and only 13% thereafter. Among workers in establishments with 500+ employees, 38% have access prior to age 65, and only 32% thereafter. In many cases, these benefits are capped at fixed dollar amounts.

These pension and retiree healthcare comparisons are summarized in Tables 8 and 9 following [47]:

[44] FERS was not enacted into law until 1987. Congress halted new enrollment into the CSRS in 1983, but did not determine the structure of FERS until 1987. During the transition period between 1983 and 1987, federal employees were offered a transition plan called CSRS Offset, which consisted of a modified CSRS pension and Social Security benefits.

[45] Office of Inspector General, United States Postal Service, “Postal Service Retirement Benefits Benchmarking,” Report Number HR-WP-14-002 (May 1, 2014), page 2.

[46] BLS Employer Costs for Employee Compensation – September 2016.

[47] National Compensation Survey: Employee Benefits in the United States, March 2016

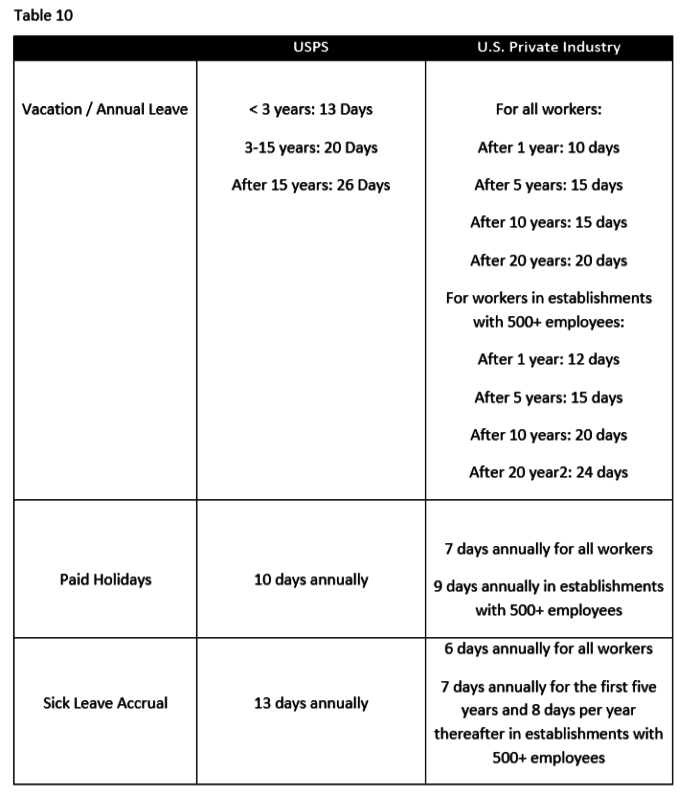

Paid Leave

Postal Service paid leave benefits are also highly generous relative to private sector norms, which can drive staffing requirements, replacement needs, and/or overtime. The following Table 10 compares USPS paid leave to BLS National Compensation Survey medians for all U.S. Private Industry workers and for those in establishments with 500 or more employees.[48]

Health Benefits (Active Employees)

By federal statute, active Postal Service workers participate in the Federal Employees Health Benefits Program (“FEHBP”), with employer contributions toward premium costs collectively bargained with the Postal Service unions. Overall, these active employee health benefits are more costly than private industry, and the Postal Service’s subsidy toward premium costs is larger than that provided by the federal government for its own employees within the FEHBP.

For Plan Year 2016, Postal Service workers represented by the APWU paid 24% of the weighted average premium costs for all levels of coverage (self, self plus one, and family), rising to 25% in Plan Year 2017, 26% in FY2018, and 27% in FY2019. Similarly, both the National Rural Letter Carriers’ Association (“NRLCA”) and National Postal Mail Handlers Union (“NPMHU”) employee premium contributions phase up to 27% by 2019. For the largest Postal Service union, the National Association of Letter Carriers (“NALC”), contributions remain at 24% based on the most recent contract that expired in 2016.[49] In the same FEHBP, most federal government employees and annuitants as of 2017 contribute the greater of 28% of the program-wide weighted average of premiums in effect each year or 75% of the total premium for the particular plan an enrollee selects.[50]

In U.S. private industry, the March 2016 BLS National Compensation Survey reported that employees typically contributed 32% of premium costs for family medical coverage (25% among large establishments with more than 500 workers) and 21% for individual coverage (20% among large establishments). According to the BLS ECEC report, employers across all industries in 2016 spent $2.44 per hour worked on health insurance.[51] In FY2016, based on analysis of the Postal Service National Payroll Summary, the USPS contributed approximately $3.71 per employee hour worked.[52]

[48] Bureau of Labor Statistics, U.S. Department of Labor, National Compensation Survey, March 2016 (www.bls.gov/ncs/)

[49] Employee premium contributions shown reflect the standard employee contribution, based on the weighted average cost of premiums across available plans. In some cases, subject to caps on the employer contribution also included in each collective bargaining agreement, contributions as a percentage of the premium cost for particular plans selected will vary.

[50] FEHB Handbook https://www.opm.gov/healthcare-insurance/healthcare/reference-materials/reference/cost-of-insurance/

[51] ECEC, September 2016

[52] National Payroll Summary, 2016

X. Recruitment and Retention

The extraordinarily low turnover experience of USPS workers and relative ease of filling vacant positions provide further strong indication that current Postal Service compensation substantially exceeds market levels. As Dr. Wachter testified before the 2003 President’s Commission, as a complement to his analysis of comparative economic labor market data:

“[W]e concluded that a significant wage premium exists. If this conclusion is correct, two implications follow. First, postal workers should have relatively low quit rates. All other factors being the same, dissatisfied workers quit their jobs. Second, the Postal Service should find it easy to hire qualified workers to fill job vacancies. In addition, if both of these factors can be shown, then the converse is also true. Unusually low quit rates and long employment queues imply the existence of a compensation premium.”[53]

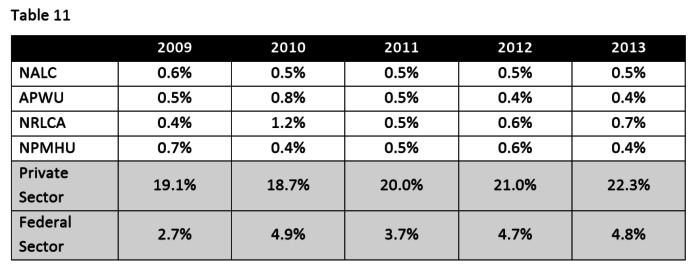

As shown in Table 11, a 2015 USPS OIG report cited annual voluntary resignations among career service workers prior to retirement (“quit rate”) at less than 1% of the workforce across the major bargaining units, far below equivalent rates cited for the private and federal sectors.[54]

The 2016 APWU arbitration award also cited similar trends of less than 1.0% quit rates for senior career employees and less than 5.0% for newer hires among members of that major Postal Service bargaining unit. As the neutral chair of the arbitration panel wrote:

“To be sure, wages and benefits are not the only considerations that enter into an employee’s decision whether to stay with the Postal Service or go elsewhere, but it would be naïve to believe that these are not major considerations. Hence, I conclude that the almost total unwillingness of APWU-represented employees to leave their jobs voluntarily is powerful evidence that they view their compensation and benefits as superior to what they would receive elsewhere, based on their skill and experience.” [55]

While quit rates for non-career employees are markedly higher than for career service employees, such increased turnover is to be expected for what are essentially temporary positions with no job security, limited benefits, and inflexible and unpredictable schedule demands associated with the use of these employees as last minute fill-ins for absences. Within the Postal Service, the USPS OIG has found that these inherent challenges are often compounded by insufficient mentoring and training non-career employees, as well as negative supervisory relationships.[56] At the same time, in evaluating non-career employee turnover, the OIG report cited three separate findings indicating that pay is not a major driver of non-career employee resignations: [57]

- First, analysis of USPS exit surveys of non-career employees for FY2016 (through July 2016) found that pay ranked 9th out of 11 reasons given for resignation, cited by only 6.24% of those separating. Ranking ahead of pay were: “Lack of schedule flexibility;” “Didn’t like supervisor;” “Physical demands;” “Too many hours;” “Not enough hours;” “Lack of advancement opportunities;” “Lack of benefits;” and, “Wasn’t trained.”

- Next, the OIG conducted its own web-based survey, and similarly found pay to rank behind “Supervisor not treating people with respect/Poor management skill,” “Lack of schedule flexibility,” and Lack of benefits” among the top reasons non-career employees have resigned.

- Finally, the OIG conducted in-depth interviews with current non-career employees, and again found issues including “Lack of flexibility,” “Lack of training,” and “Supervisor not treating people with respect” to rank well above compensation among the top concerns with their positions.

Consistent with these findings, the Postal Service has also stated that:

“Most frequently cited causes for non-career employee turnover are lack of schedule flexibility, physical demands, and employee did not like supervisor.”[58]

While such non-economic issues are of concern, and may represent further opportunities for workforce cost savings if successfully addressed to reduce non-career employee turnover and replacement costs, there is no indication that the pay rates for these positions are inadequate. To the contrary, the Postal Service’s success in routinely filling approximately 130,000 non-career positions nationally despite these limitations indicates the attractiveness and market competitiveness of Tier 2 pay rates for the type of work performed.

[53] Wachter testimony, page 7.

[54] USPS OIG RARC-WP-15-004, “Flexibility at Work: Human Resource Strategies to Help the Postal Service,” January 5, 2015, page 12.

[55] APWU 2016 Award, pages 7-8, and 11.

[56] USPS OIG “Non-Career Employee Turnover,” HR-AR-17-002, December 20, 2016, pages 1-2.

[57] USPS OIG “Non-Career Employee Turnover,” HR-AR-17-002, December 20, 2016, pages 7-9.

[58] Responses of the United States Postal Service to Questions 4-7 and 10 of Chairman’s Information Request No. 14, Annual Compliance Review 2016, February 15, 2017, page 3.

XI. Past USPS Cost Containment Efforts and Remaining Untapped Opportunity

Past partial cost containment measures negotiated by the USPS, primarily impacting newly hired personnel, have demonstrated the potential for significant compensation restructuring and savings if built upon and further expanded. For the majority of on-board Postal Service employees, however, wage growth has continued to outpace consumer price growth as well as federal employee wage gains, despite the long-documented presence of the wage premiums outlined above. Going forward, strengthened controls represent a strong and largely untapped opportunity to moderate cost growth prospectively.

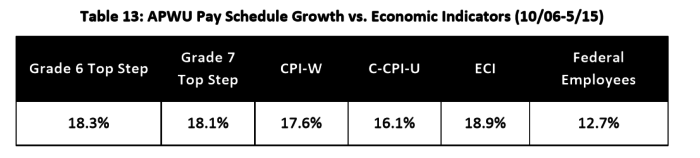

USPS Wage Trends for Incumbent Employees